Does a car trade-in count as a down payment? Practical guide — CarFax Deals

This guide explains when a trade in car functions like a down payment, how to calculate net equity, and what to verify with the dealer. It shows the payoff calculation buyers should use and how state sales tax rules can change out-of-pocket costs.

A step-by-step workflow for estimating a truck's market value that centers on comparing consumer valuation tools, adjusting for mileage and condition, and checking wholesale market signals. The guide explains private-party, trade-in and dealer retail values and shows how a vehicle history report and pricing insights can change an asking price.

This guide helps research oriented buyers evaluate suv used cars for sale under $25,000 by combining safety ratings, reliability data, local pricing context, and vehicle history checks. It outlines a simple framework, a pre visit checklist, and a decision scoring worksheet so you can compare finalists before contacting a dealer. Use the steps here to narrow candidates and confirm risk signals with a vehicle history report and a pre purchase inspection.

When searching suv used cars for sale, prioritize model year, trim and powertrain before choosing a make or model. This guide explains how safety ratings, dependability studies and local pricing insights combine to produce a short list you can verify with a vehicle history report. It also provides a stepwise checklist you can use before contacting a dealer.

If you plan to trade in your current vehicle when buying another, understanding how that trade-in affects the transaction can save you surprises at signing. This article explains when a trade in car functions like a down payment, how to calculate net equity, and what to check with the dealer before you agree to the offer.

We use simple formulas and practical steps so you can estimate the cash you will need and how the trade-in may change monthly payments. The goal is to help you verify dealer figures and confirm tax treatment before you finalize a deal.

A trade-in can act like a down payment because dealers usually apply the vehicle's value against the purchase price or to clear an existing loan.

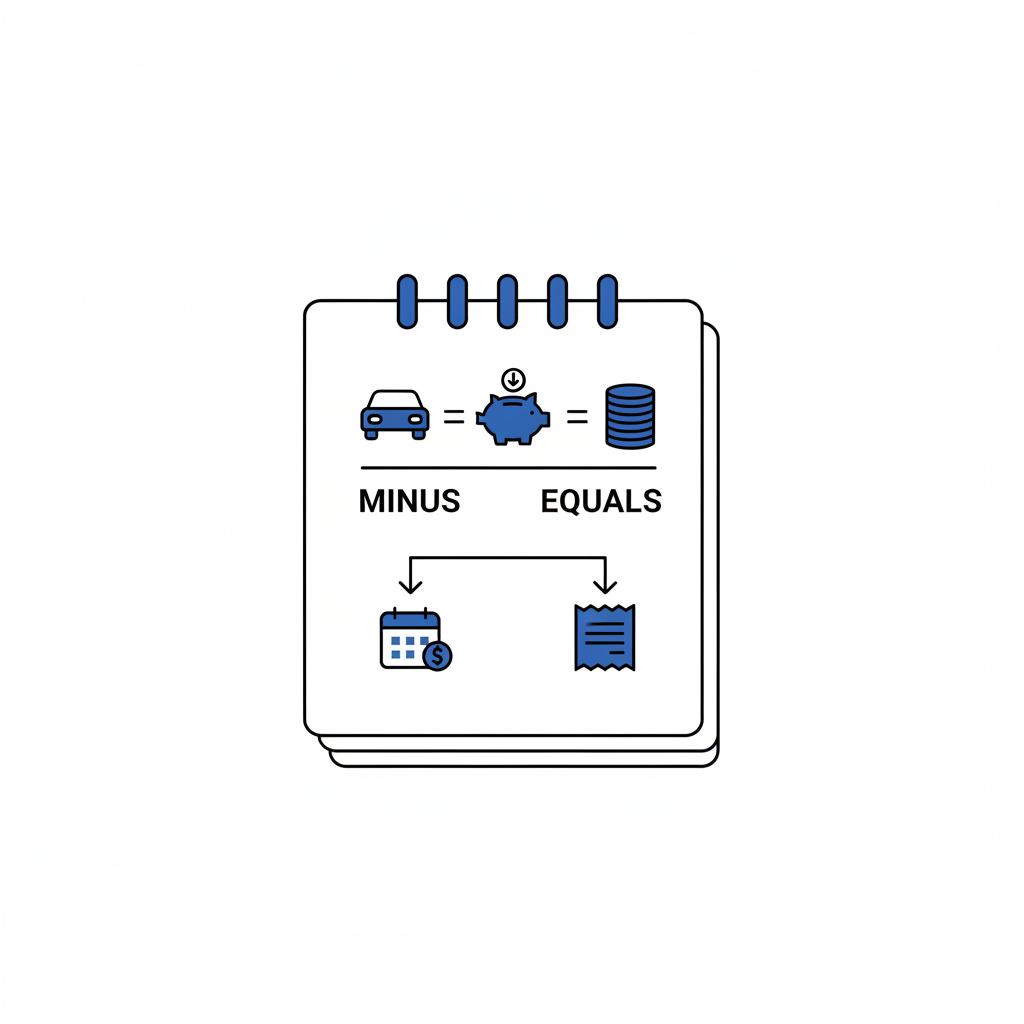

Net equity equals trade-in offer minus payoff; positive net equity reduces cash needed, negative equity raises the financed amount.

State sales-tax rules vary, so confirm whether your state allows a trade-in credit before assuming tax savings.

Does a trade in car count as a down payment? Quick definition and key idea

When a trade in car is treated like a down payment

A trade in car often counts as a down payment because dealers apply the vehicle's value against the purchase price or use it to pay off an existing loan, which reduces the amount you must finance.

In practical terms you do not hand over cash at signing when the trade-in has positive net equity; instead the dealer credits that value toward the purchase, and the net equity is what lowers your required cash or financed amount, depending on the deal.

Net equity is the simple math: trade-in offer minus outstanding payoff equals net equity; positive net equity lowers the cash you need, while negative equity means you owe the difference or the dealer may roll it into the new loan, increasing the financed amount and monthly payments. Edmunds explanation of trade-ins

Sales tax rules vary by state and can change the out-of-pocket effect of a trade-in, because some states calculate sales tax on the purchase price after the trade-in credit while others do not, so check local guidance before assuming the trade-in will lower total taxes.

This explanation follows common consumer guidance that describes dealer payoff handling and buyer protections and helps you understand why asking for a payoff statement matters when you expect a trade-in to act like a down payment. CFPB guidance on trade-ins

How dealers actually apply a trade-in to your purchase

The dealer process usually begins with an appraisal of your vehicle to produce a trade-in offer; next the dealer checks the loan payoff, and then applies the net equity as a credit against the purchase price or to clear the existing loan.

Appraisal, payoff, and credit application often happen in that order, and the key number to watch is the payoff the dealer will actually send to your lender; getting that number in writing helps you confirm the net equity the dealer is using.

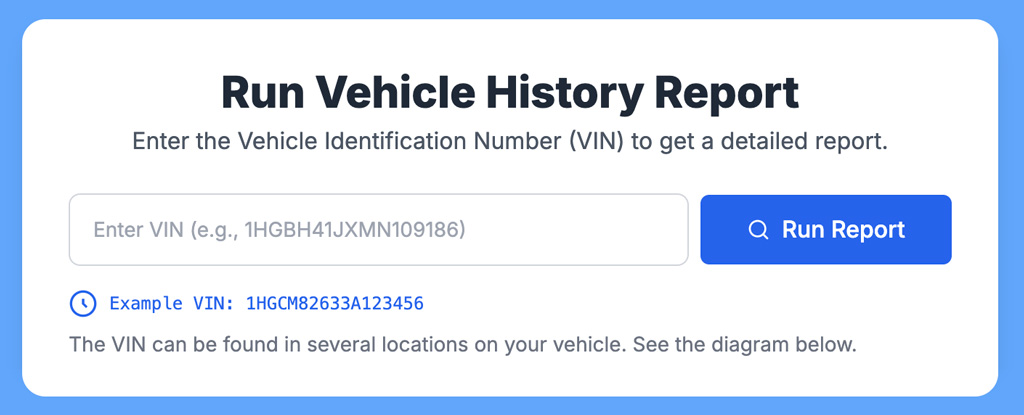

Run a vehicle history report before finalizing a trade-in

Ask the dealer for a written payoff statement and request that the trade-in offer be listed on the sales paperwork.

Dealers generally handle paying off the current loan before title transfer, and you should verify timing and amounts because the net equity depends on the offer and the exact payoff figure; request a payoff statement and keep a copy for your records. FTC guidance on dealer paperwork

If you owe more than the vehicle is worth, the dealer may require extra cash to cover the shortfall or may offer to roll that negative equity into the new loan, which raises the financed amount and often the monthly payment. Bankrate overview of negative equity

Expect specific paperwork items such as the dealer's trade-in offer, the payoff statement, title assignment forms, and the sales contract showing how the trade-in was applied; review each item before signing to confirm the trade-in reduced the financed amount as you expect. Edmunds on trade-in paperwork

How to estimate your trade-in's impact on monthly payments

Start with the basic formula: trade-in offer minus loan payoff equals net equity; then subtract positive net equity from the cash down payment you would otherwise need, or add negative net equity to the new loan amount. Edmunds net equity method

Example scenarios make this concrete. For modest positive equity, imagine a trade-in offer of 8,000 and a payoff of 6,000, producing 2,000 net equity that lowers the cash required at signing or reduces the financed amount by 2,000.

For zero equity, a trade-in offer equal to the payoff does not change the cash or financed amount; you get value in convenience but not in reduced payments unless taxes or fees differ.

For negative equity rolled into a loan, suppose the trade-in offer is 5,000 and the payoff is 7,000, leaving negative equity of 2,000 that the dealer may add to the new loan, increasing the principal and thus monthly payments. Kelley Blue Book on trade-in value impacts

The final monthly payment also depends on the new loan's interest rate and term; even a sizable trade-in that reduces principal can leave payments high if the new loan's rate is higher or the term is extended to lower the payment but increase total interest. Bankrate on loan term and rate effects

Always verify dealer figures against the payoff statement and a written loan estimate before signing; comparing those numbers to your own calculations helps ensure the trade-in produces the expected change in monthly payments. Edmunds payoff verification advice

State sales tax and trade-ins: what changes your out-of-pocket cost

Have you checked how your state calculates sales tax when a trade-in is applied?

A trade in car can count as a down payment because dealers usually apply the vehicle's value against the purchase price or use it to pay off an existing loan; the net equity determines how much it reduces cash or increases financing.

Because state rules vary, ask the dealer to show the tax calculation in writing and confirm whether the trade-in lowered the taxable amount on your contract; if you are unsure, check the state department of taxation or motor vehicles for official guidance. FTC note on tax and dealer disclosures

If the dealer applies a trade-in credit for tax purposes, the immediate out-of-pocket cost can be lower than a same-price cash purchase; if the state does not allow a trade-in credit then the tax benefit may not appear and the trade-in may only affect financing. California tax rules as an example

Negotiation and dealer practices: common pitfalls with trade-ins

Dealer appraisals often differ from private-sale value because dealers price vehicles for retail inventory, reconditioning costs, and local demand, so expect a lower trade-in offer than a well-executed private sale might bring. KBB on appraisal vs private sale

Negative equity can be obscured by monthly payment math; a dealer may show a lower monthly payment by extending the loan term while folding negative equity into the balance, so compare total financed principal and the loan schedule rather than focusing only on the monthly figure. Bankrate on negative equity and payments

Common fees and timing issues include unpaid lender fees, dealer payoff processing time, and any reconditioning charges the dealer deducts from the trade-in offer; ask the dealer to list deductions and to show the payoff timing before you accept the offer. Edmunds on fees and timing

Get independent estimates and a vehicle history report to support your position in negotiation; presenting documentation that shows clean title, ownership history, or recent maintenance can help explain a higher private-market value even if dealers still offer less for trade-in. CFPB advice on documentation

Step-by-step checklist: prepare, appraise, and close the trade-in

Before you visit a dealer, gather an up-to-date payoff amount from your lender, get independent trade-in estimates, and obtain a vehicle history report to confirm title status and ownership records.

Run CarFax Report for a vehicle history report that can help confirm ownership and title status when you seek independent valuations.

At appraisal, present your documentation and ask for a written trade-in offer that lists any deductions; compare this offer to independent estimates so you know whether the dealer's number is within a reasonable range. Edmunds appraisal guidance

Before you sign, confirm the payoff amount and timing, verify how the dealer calculated tax with the trade-in, and ensure any negative equity treatment is shown in writing on the contract; do not sign until you see the numbers you verified. FTC used car paperwork guidance

Common mistakes to avoid when using a trade-in

1. Do not assume the dealer will handle payoff the way you expect; always request a written payoff statement from the lender or ask the dealer to provide their planned payoff timeline and amount. CFPB on payoff verification

2. Do not rely solely on a dealer appraisal; get independent valuations and a vehicle history report to support your expected value and to highlight ownership or title details that affect price. KBB on independent valuation

3. Check state tax treatment early; asking the dealer how tax will be calculated with a trade-in can prevent surprises when the contract shows a different taxable amount than you expected. State tax example guidance

Final checklist and next steps: can you rely on a trade-in as a down payment?

estimate net equity and monthly payment change

Use to check financed amount

Recap the net equity formula: trade-in offer minus outstanding payoff equals net equity; positive net equity reduces required cash, negative net equity increases what you must finance unless covered by cash at signing. Edmunds net equity recap

Final actions: get a written payoff, secure independent trade-in estimates, and confirm how taxes and fees will be calculated; keep all payoff statements and the final dealer contract for your records and revisit numbers if anything changes before funding. CFPB consumer guidance (check your state tax agency: Indiana DOR sales tax)

Not always. The trade-in reduces financing only by the net equity, which is the trade-in offer minus the outstanding payoff. If net equity is negative, you may need cash or the shortfall may be rolled into the new loan.

It depends on state rules. Many states allow a trade-in credit so tax is calculated on the net price after the trade-in, but you should confirm the method with the dealer or the state revenue office.

Ask for the written trade-in offer, the dealer's payoff statement or payoff timing, and the contract showing how the trade-in and taxes were applied. Keep copies of every document.

A trade-in often reduces the cash you need at signing, but the exact effect depends on net equity, dealer payoff handling, and state tax rules. Take the time to collect written payoff figures, independent valuations, and a clear tax calculation so the trade-in works as you expect.

Keep copies of all payoff statements and the sales contract. If numbers change, revisit the deal before you sign or fund the loan.